Close Menu

Close Menu

Vaishali Pant

Technology

BENEFITS OF BLOCKCHAIN: The Advantages of Blockchains

Vaishali Pant

Vaishali Pant

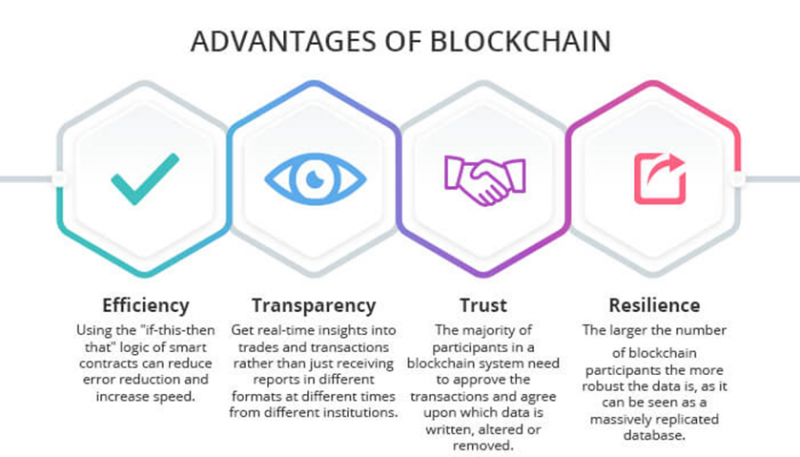

Let us discuss Benefits of blockchain: The Advantages Of Blockchain

1. Transaction Accuracy on the Blockchain

A network of thousands of computers approves transactions on the blockchain network. This virtually eliminates human intervention in the verification process, resulting in lower human error and a more accurate record of data. Even if one of the computers on the network committed a computational error, it would only affect one copy of the blockchain. For that error to spread to the rest of the blockchain, at least 51 percent of the network's computers would have to make it—a near-impossibility for a big and rapidly developing network like Bitcoin's.

2. Reduced Costs

Consumers typically pay a bank to verify a transaction, a notary to sign a document or a preacher to marry them. The blockchain eliminates the need for third-party verification, as well as the fees that come with it. When a business accepts credit card payments, for example, it pays a tiny charge to the banks and payment-processing businesses to handle the transactions. Bitcoin, on the other hand, has no central authority and only has a small number of transaction fees.

3. Decentralization

Blockchain doesn't save any of its data in a single location. Instead, a network of computers copies and spreads the blockchain. Every computer on the network updates its blockchain to reflect the addition of a new block to the blockchain.

Blockchain makes it more difficult to tamper with data by disseminating it across a network rather than holding it in a single central database. If a hacker obtained a copy of the blockchain, just a single copy of the data would be compromised, rather than the entire network.

4. Transactions that are quick and easy

The settlement of transactions made through a central authority can take many days. For example, if you deposit a check on Friday evening, you may not see funds in your account until Monday morning. Blockchain operates 24 hours a day, seven days a week, and 365 days a year, unlike financial institutions, which function during business hours, which are normally five days a week.

5. Transactions in Confidentiality

Many blockchain networks function as public databases, allowing anybody with an Internet connection to access the network's transaction history. Although users have access to transaction details, they do not have access to identifying information about the people who are conducting the transactions. It's a frequent misconception that blockchain networks like bitcoin are anonymous, but they're not.When a user conducts a public transaction, their unique code—referred to as a public key—is published on the blockchain. Their personal information, on the other hand, isn't. If a person purchases Bitcoin on an exchange that demands identification, their identity is still tied to their blockchain address.

Source:

Click for the: Full Story

You might like

You Might Like this